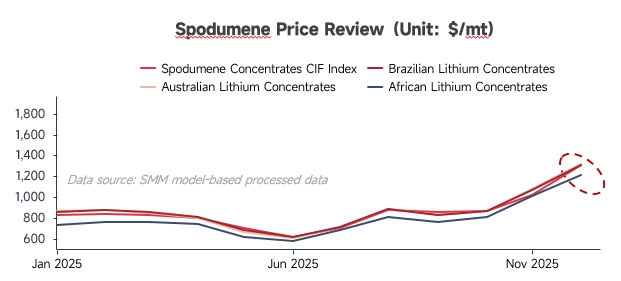

Price Review

In the first half of 2025, lithium ore prices continued to decline. Upstream mining companies adopted a "ship first, sell later" strategy, while persistent efforts to maintain high prices led to elevated inventories of lithium concentrate at ports. On the demand side, weak spot and futures prices for lithium carbonate reduced production enthusiasm among non-integrated lithium salt plants, keeping their operating rates at low levels. Overall market transactions were subdued, with prices once falling close to the cost line of mining companies.

In the second half of 2025, driven by supply disruptions from domestic mines and robust downstream demand, lithium prices rebounded significantly. Upstream mining companies and holders seized the opportunity to raise prices, effectively boosting market sentiment. By the late third quarter, influenced by shipping schedules and overseas supply constraints, domestic circulation volumes tightened noticeably against the backdrop of increased operating rates at non-integrated lithium salt plants. Coupled with the rising frequency and higher prices of overseas mine auctions, these factors collectively drove spodumene concentrate prices to their current elevated levels.

Supply Side

1. Spodumene Mines

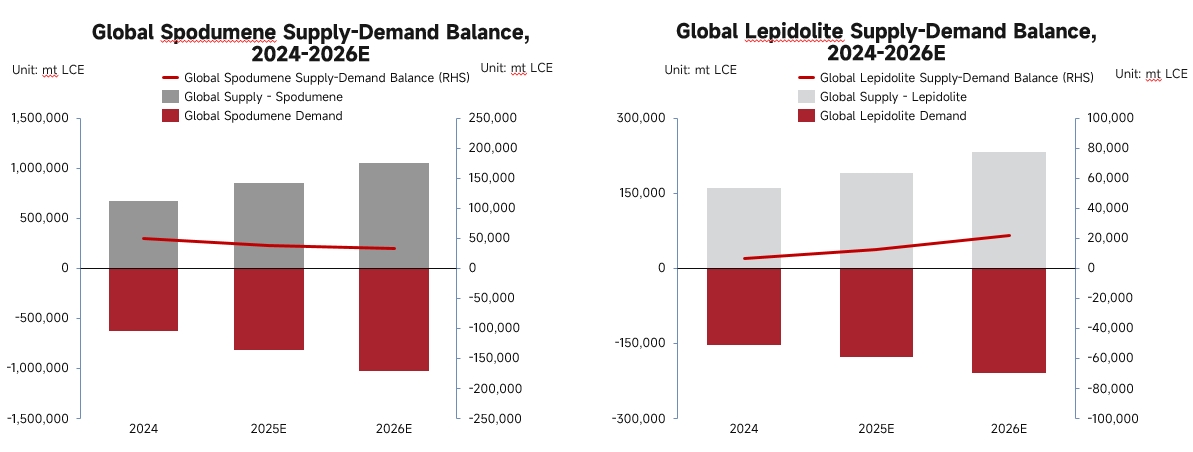

In 2025, global spodumene mine supply exceeded 850,000 tonnes LCE, a significant year-on-year increase of 27%.

Australian Mines: Established mines maintained stable output. Although they experienced a price low in mid-year, some mines with cost advantages slightly raised their production guidance after prices recovered in Q3.

African Mines: Most Chinese-owned mines in Zimbabwe operated steadily, with a few expanding production as planned and constructing lithium sulfate refineries to respond to the country's gradually tightening export policies. Mali emerged as a new supplier, with its lithium project holders gradually establishing transportation routes in the second half of the year and beginning to ship processing raw materials to China. **Nigeria:** Supply volume increased year-on-year in 2025, but full-year supply stability was relatively weak due to its domestic policies.

China Domestically: In Xinjiang, the completion of high-capacity processing plants significantly improved beneficiation efficiency. Operating mines in Sichuan achieved higher capacity utilization rates and have plans for further production increases. Additionally, new projects are progressing through procedures such as mining license approvals.

2. Lepidolite Mines

In 2025, lepidolite supply exceeded 180,000 tonnes LCE, with a year-on-year growth rate exceeding 18%. The main increment came from continuous production increases by leading lithium salt producers in Jiangxi province during Q2-Q3. However, their supply halted in the second half of the year due to mining license disputes, introducing volatility to overall lepidolite ore supply. Apart from scheduled maintenance at other operating mines in Jiangxi throughout the year, overall production remained stable. An integrated mining, beneficiation, and smelting project for lepidolite in Hunan was completed and put into operation at year-end, with volume expected to ramp up steadily going forward. The mining, beneficiation, and comprehensive utilization project for lepidolite in Inner Mongolia has established stable production capacity and is focused on building a closed-loop industrial chain from ore to batteries.

Demand Side

In 2025, global smelting demand for lithium ore exceeded 980,000 tonnes LCE, representing a year-on-year increase of 28%. The primary driver of this growth was robust demand for lithium carbonate smelting, while demand for lithium hydroxide smelting remained relatively weak.

Supply-Demand Balance

In 2025, global lithium resource supply grew steadily, supported by efficiency improvements in existing project capacities and the concentrated commissioning of new projects. On the demand side, driven by high spot and futures prices in the second half of the year, operational enthusiasm rose significantly, maintaining rigid growth. The global lithium ore supply-demand balance in 2025 continued to tighten compared to 2024, with lepidolite experiencing greater tightness due to its concentration among leading suppliers.

Looking ahead, the cycle of project expansions and commissioning is expected to conclude within the 2026 timeframe. New projects added in recent years will gradually ramp up and release capacity during 2026-2027, pushing upstream lithium ore output beyond 1.28 million tonnes LCE. Downstream demand, particularly driven by growth in the energy storage segment, is expected to keep ore demand high, exceeding 1.23 million tonnes LCE. Although the overall lithium ore market may show a slight surplus, it will continue to tighten compared to 2025. It is worth noting, however, that the balance could be disrupted by weather-related or policy-induced supply shocks in major producing regions.

Looking ahead, the cycle of project expansions and commissioning is expected to conclude within the 2026 timeframe. New projects added in recent years will gradually ramp up and release capacity during 2026-2027, pushing upstream lithium ore output beyond 1.28 million tonnes LCE. Downstream demand, particularly driven by growth in the energy storage segment, is expected to keep ore demand high, exceeding 1.23 million tonnes LCE. Although the overall lithium ore market may show a slight surplus, it will continue to tighten compared to 2025. It is worth noting, however, that the balance could be disrupted by weather-related or policy-induced supply shocks in major producing regions.